The Arbitration Trap

How the No Surprises Act removed patients from billing disputes and replaced them with a government arbitration pipeline no one was prepared to operate.

2024 Disputes Filed

1.46M

initiated in one year

Original Estimate

17,000

per year (CMS, 2022)

Provider Win Rate

80%

of closed disputes (2023)

PE Firm Share

67%

of all 2023 disputes

The No Surprises Act, effective January 1, 2022, prohibits balance billing for emergency services, non-emergency services at in-network facilities by out-of-network providers, and air ambulance services. When providers and insurers disagree on payment, the law routes the dispute through a Federal Independent Dispute Resolution (IDR) process. The government estimated 17,000 disputes per year. In 2024, providers filed 1.46 million. The system was never designed for this volume, and the players who dominate it are not the physicians the law was meant to help.

What the Law Was Supposed to Do

Remove patients from the crossfire of out-of-network billing disputes. On that narrow promise, it delivered.

The Patient Protection

Before the NSA, patients caught in out-of-network emergencies faced "surprise bills" — the difference between what their insurer paid and what the provider charged. These bills could reach tens of thousands of dollars for a single ER visit.

The law fixed this by capping patient cost-sharing at in-network rates and routing the payment dispute to arbitration between the provider and insurer. AHIP estimates the law has prevented more than 1 million surprise bills per month since January 2022.

That is the success story. Everything that follows is the failure.

The Unintended Consequence

The law didn't eliminate billing disputes. It centralized them into a government arbitration pipeline. The patient was removed from the equation, but the economic conflict between providers and insurers was compressed into a single bottleneck: the Federal IDR process.

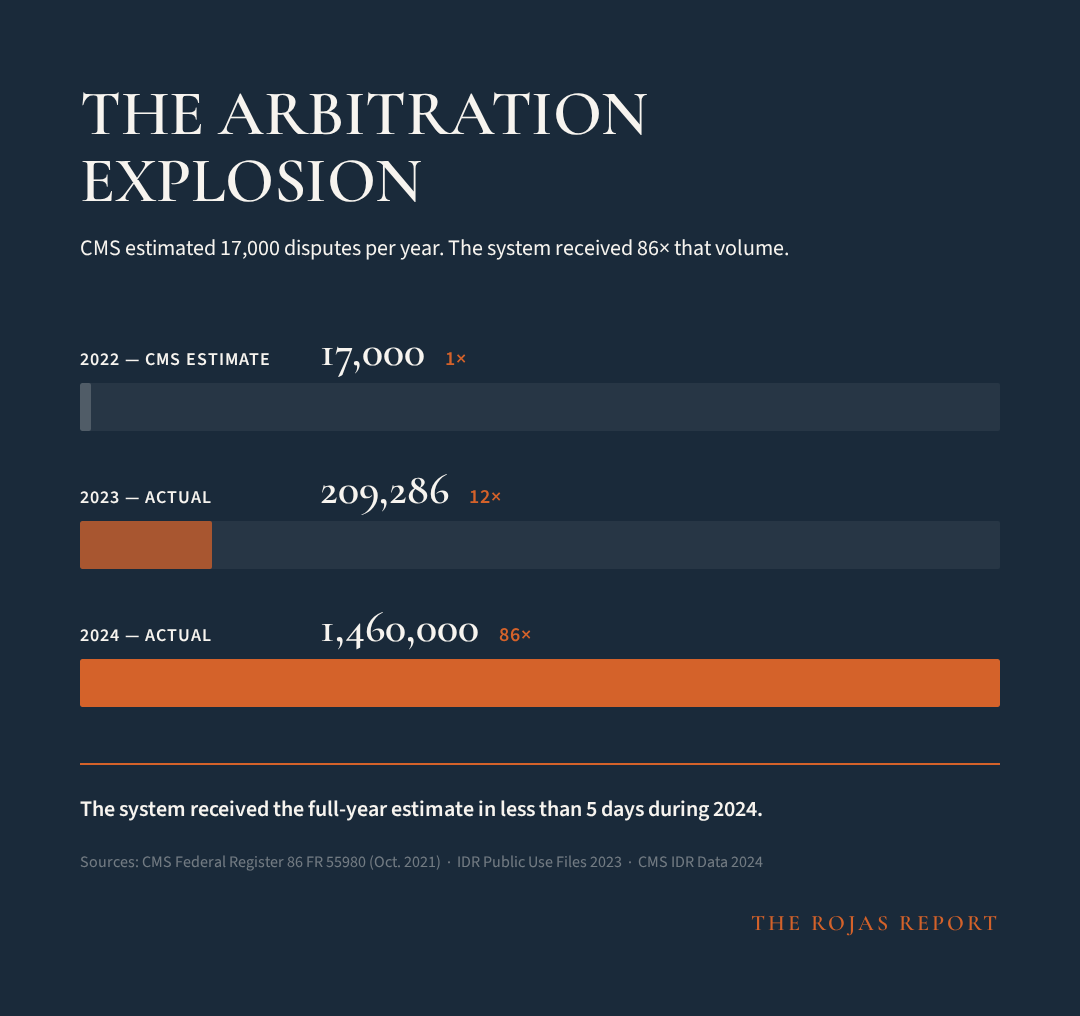

86x the Estimate

CMS predicted 17,000 disputes per year. The system received 1.46 million in 2024. This is not a rounding error. It is a structural miscalculation.

The Escalation

2022 (CMS Estimate)

2023 (Actual — PUF Data)

2024 (Actual — CMS)

Sources: CMS Federal Register 86 FR 55980 (Oct. 2021); IDR Public Use Files 2023; CMS IDR data 2024.

Infrastructure Gap

The IDR portal, certified IDR entities, and administrative staff were scaled for 17,000 annual disputes. The system received that many in less than 5 days during 2024.

Processing Delays

By Q4 2023, the mean time to close a dispute was 102 business days. Air ambulance disputes averaged 139 business days. The statutory target is 39.

Multiple Pauses

The IDR process was paused multiple times in 2023 due to court decisions in the Texas Medical Association litigation, further extending backlogs.

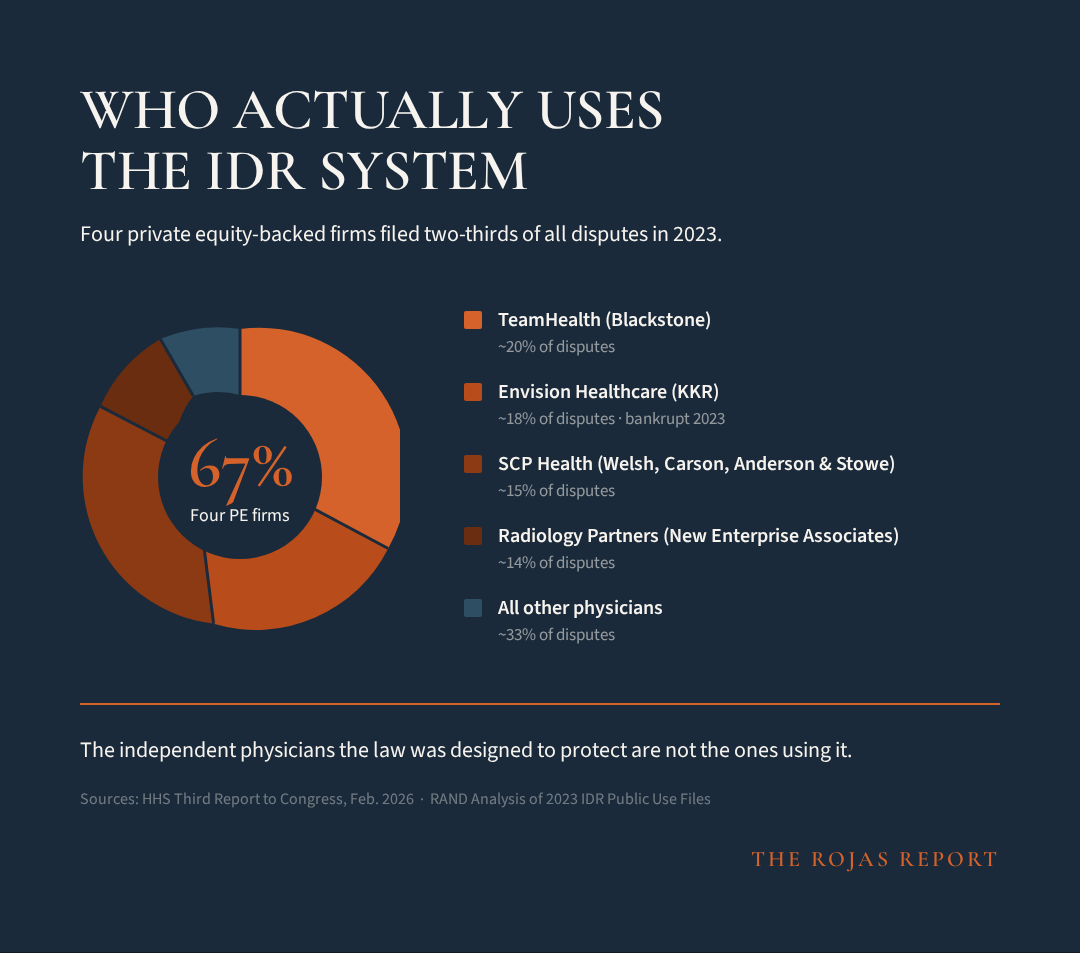

Four PE Firms. Two-Thirds of All Disputes.

The IDR system is not being used by the independent physicians it was designed to protect. It is being industrialized by private equity.

The Dominant Filers (2023 IDR PUF Data)

Four large firms affiliated with private equity funds filed over two-thirds of all IDR disputes closed in 2023. Three are the largest emergency medicine staffing companies in America. The fourth is the largest radiology staffing firm.

TeamHealth

Emergency Medicine — PE Owner: Blackstone

~20%+

Envision Healthcare

Emergency Medicine — PE Owner: KKR (bankrupt 2023)

~18%+

SCP Health

Emergency Medicine — PE Owner: Welsh, Carson, Anderson & Stowe

~15%+

Radiology Partners

Radiology — PE Owner: New Enterprise Associates

~14%+

Combined

Four firms, all PE-affiliated

67%+

Source: HHS Third Report to Congress, February 2026. RAND analysis of 2023 IDR Public Use Files.

Air Ambulance: Even More Concentrated

For air ambulance IDR disputes, concentration is even more extreme: five large provider groups filed 87.7% of all disputes. Providers won approximately 85% of air ambulance arbitrations. The median QPA for a rotary wing air transport was $13,684 — payment determinations were markedly higher.

The Specialty Breakdown

Emergency medicine represents 60% of IDR disputes but only 11% of OON claims — a 5.5x overrepresentation.

Seven Ways Insurers Circumvent the Law

Court rulings, regulatory findings, and IDR system data reveal a systematic pattern of insurer tactics that undermine the statute's intent.

Artificially Low QPA Benchmarks

Insurers calculate the Qualifying Payment Amount (QPA) themselves. That number becomes the anchor in arbitration. The underlying data is not transparent to providers. Federal courts repeatedly ruled regulators implemented rules that effectively favored insurer QPAs, contradicting the statute.

Texas Medical Association v. HHS — Fifth Circuit confirmed nothing in the law allows weighting QPA more heavily than other factors.

Underpay First, Force Arbitration Later

Insurers pay extremely low initial reimbursements knowing most providers won't pursue IDR due to filing costs, administrative burden, and time delays. Even lawyers specializing in NSA arbitration note insurers rely on 'artificially low QPAs to justify reduced offers.' Many claims are simply absorbed.

Structural: IDR filing costs + 91-day mean resolution time = economic deterrent for small practices.

Massive Eligibility Challenges

Insurers frequently challenge whether claims qualify for IDR at all. Over one-third of claims faced eligibility challenges in the first year. These challenges delay payment and can knock claims out of arbitration entirely.

CMS data: 300,000+ disputes filed in Year 1, over 1/3 faced eligibility challenges.

Refusing Payment After Arbitration

Even when arbitrators issue binding decisions, insurers sometimes delay or refuse payment. IDR determinations are legally binding, yet payors have refused to pay after determinations. The law has limited enforcement mechanisms.

Legal commentary and provider reports documented in HHS stakeholder interviews.

Cost-Prohibitive Arbitration Fees

Administrative IDR fees increased 600% before courts invalidated the rule. High fees discourage smaller physician groups from filing disputes — exactly the providers who need the system most.

Administrative fee went from $50 to $350 before court intervention. IDRE fees range $200–$1,340.

Technical Eligibility Loopholes

Some payers argue certain claims are not NSA-eligible due to plan-year timing or coding interpretations. Claims denied IDR eligibility because the insurance plan year had not started yet, even though the service occurred after the law took effect.

Documented in legal analysis of IDR eligibility disputes.

Network Exclusion Revenue Sharing

Some insurers use third-party network management firms that receive shared savings revenue under network exclusions — financially rewarding firms for out-of-network services. Multiple benefit consultants noted the conflict of interest inherent in this arrangement.

HHS Third Report to Congress, February 2026 — stakeholder interviews.

The Legal Record

Three separate federal court rulings in Texas Medical Association v. HHS sided with physicians because the implementation favored insurers. The courts struck down the QPA presumption, invalidated batching restrictions, and invalidated excessive IDR fees. That litigation is the clearest public record that the system was structurally tilted toward insurers.

Arbitration by the Numbers

When providers win 80% of disputes, the question isn't whether the system works — it's why insurers underpay in the first place.

QPA vs. Payment Determination: The Spread

The Qualifying Payment Amount (QPA) — calculated by the insurer — consistently anchors below what arbitrators ultimately award. For the most commonly disputed emergency medicine code, the median payment determination was 2.3x the median QPA.

99284

Emergency Dept Visit (High Severity)

Median QPA

$229

Median Award

$529

Ratio

2.3x

00812

Anesthesia for Colonoscopy

Median QPA

$276

Median Award

$790

Ratio

2.9x

71045

Chest X-Ray (1 view)

Median QPA

$9

Median Award

—

Ratio

—

A0431

Rotary Wing Air Transport

Median QPA

$13,684

Median Award

>>QPA

Ratio

Markedly higher

Source: RAND analysis of 2023 IDR Public Use Files. HHS Third Report to Congress, February 2026.

The Cost of Arbitration

Who Pays the Plans

The majority of IDR disputes involve self-insured employer plans — meaning the employer, not the insurance company, ultimately bears the cost of higher arbitration awards.

Priced Out of Their Own Protection

The law was written to protect physicians from surprise billing disputes. The implementation ensures only the largest firms can afford to use it.

What HHS Found

The HHS Third Report to Congress (February 2026) documented that smaller provider groups reported they were not using the Federal IDR process due to:

Cost of participation

Filing fees, legal costs, and administrative overhead make individual dispute filing uneconomical for small practices

Length of time to determination

91-day average (139 days for air ambulance in Q4 2023) means cash flow disruption for practices operating on thin margins

Delays in receiving payment

Even after winning, providers must chase payment — enforcement mechanisms are limited

The Industrial Advantage

PE-backed firms can industrialize IDR workflows because they have:

Dedicated legal and billing teams for dispute filing

Volume to batch disputes and reduce per-claim costs

Capital to absorb 91+ day payment delays

Negotiating leverage from controlling 67% of the dispute pipeline

Data infrastructure to track QPA patterns across markets

The result: a system designed to protect physicians from surprise billing has become a system that rewards the firms large enough to weaponize arbitration at scale.

IDR + CON + 340B: The Triple Lock

The No Surprises Act doesn't exist in isolation. It operates within the same market structure that Certificate of Need laws and the 340B program protect.

CON Laws

Limit competition by requiring government permission to build or expand healthcare facilities. 35 jurisdictions maintain these laws, protecting incumbent hospital systems from new market entrants.

Read the CON Investigation →340B Program

Provides $81.4 billion in discounted drug purchases to hospital systems with no requirement to pass savings to patients. The spread between acquisition cost and insurance reimbursement is pure margin.

Read the 340B Investigation →IDR Process

Routes 1.46 million disputes through a government pipeline where PE-backed firms dominate and independent physicians are priced out. The arbitration system rewards scale, not clinical value.

The pattern: CON laws block competition. 340B subsidizes the incumbents. The IDR process routes payment disputes through a system only the largest firms can afford to use. Each mechanism independently favors consolidated healthcare. Together, they form an interlocking architecture that systematically disadvantages independent physicians and independent practice.

The Rojas Report Take

The Rojas Report Take

The No Surprises Act is the most successful consumer protection law in recent healthcare history. It is also, simultaneously, a structural accelerant for healthcare consolidation. Both things are true, and the policy establishment's refusal to hold both ideas at once is why the implementation has been so chaotic.

The law solved the visible problem — patients receiving five-figure bills for emergency care they didn't choose. On that metric, it is an unqualified success. More than nine million surprise bills have been prevented since January 2022. That matters.

But the law didn't eliminate the underlying economic conflict. It compressed it into a single government-run arbitration pipeline and assumed the system would process 17,000 disputes per year. It received 86 times that volume. The infrastructure was never designed for this. The statutory timelines are fiction. The backlog is structural.

The deeper problem is who benefits from this compression. Four private equity-backed firms — TeamHealth, Envision, SCP Health, and Radiology Partners — filed over two-thirds of all IDR disputes in 2023. These are not independent physicians seeking fair payment. These are industrial-scale arbitration operations that have turned the dispute resolution process into a revenue extraction mechanism.

Meanwhile, the independent physicians the law was theoretically designed to protect are priced out. The filing costs, the 91-day average resolution time, the limited enforcement after winning — all of these create barriers that only well-capitalized firms can absorb. The HHS report confirms this: smaller providers reported they are simply not using the system.

The insurer side is no better. Three separate federal courts have ruled that the implementation was tilted toward insurers. The QPA — calculated by the insurer, opaque to the provider — anchors arbitration downward. Insurers underpay strategically, knowing most providers won't pursue arbitration. When they do, insurers challenge eligibility on a third of claims. When they lose, some delay payment anyway.

This is not a broken system. It is a system working exactly as the incentives predict. The law removed patients from the equation and left two well-resourced adversaries — PE-backed provider firms and insurance companies — to fight over payment rates through government arbitration. Independent physicians and their patients are bystanders to a conflict between entities that have the capital to industrialize the process.

The policy didn't remove disputes. It centralized them into a government arbitration pipeline. And the players who win are the ones who can industrialize the workflow.

Sources & Methodology

[1] HHS Third Report to Congress on the No Surprises Act, February 2026

[2] RAND Corporation analysis of 2023 IDR Public Use Files (commissioned by ASPE)

[3] CMS Federal Register 86 FR 55980 (October 2021) — original 17,000 dispute estimate

[4] Georgetown University Center on Health Insurance Reforms (CHIR), 2024 IDR data analysis

[5] Niskanen Center, 'New Data Shows No Surprises Act Arbitration Is Growing Healthcare Waste'

[6] BCBS, 'No Surprises Act Year 3 Report'

[7] Texas Medical Association v. HHS, multiple rulings (E.D. Tex. & 5th Cir.)

[8] AHIP, 'No Surprises Act Continues to Prevent More than 1 Million Surprise Bills Per Month' (2024)

[9] Health Affairs, 'A Surprise Benefit of New Billing Dispute Rule' — Patrick Velliky

All data sourced from publicly available federal reports, court filings, and peer-reviewed analysis reviewed as of March 2026.